Driven by a continuous surge in overseas orders, Chinese lithium iron phosphate (LFP) battery manufacturers are significantly ramping up their efforts to establish production facilities abroad. In early December 2024, CATL and Stellantis announced a joint venture investment of €4 billion (approximately RMB 30.6 billion) to build a massive LFP battery plant in Spain. The facility is scheduled to commence production by the end of 2026, with a planned capacity of 50 GWh.

Prior to this, CATL—China’s leading battery supplier with the largest overseas client base—had already constructed two battery plants in Europe, located in Germany and Hungary. These facilities boast a combined planned capacity exceeding 100 GWh, producing both LFP and ternary batteries primarily for European and other international automakers.

Beyond CATL, other Chinese battery giants are also expanding globally. EVE Energy, which has already broken ground on a battery plant in Hungary, saw its U.S. joint venture, ACT, begin construction on an LFP battery project in Mississippi in July 2024. The facility is expected to produce 21 GWh of prismatic LFP batteries annually, with shipments starting in 2026. Meanwhile, Envision AESC launched construction on its own LFP battery plant in Spain the same month, targeting production by 2026.

LFP material suppliers are also joining the overseas expansion wave. In October 2024, Changzhou Lithium (a subsidiary of Longpan Tech) signed a $200 million (RMB 1.45 billion) investment agreement with the Indonesia Investment Authority (INA) and other partners to expand its Indonesian plant’s annual LFP cathode material capacity from 30,000 tons to 120,000 tons.

Earlier, in September 2024, Wanrun New Energy announced plans to invest $168 million (RMB 1.22 billion) in an LFP production facility in South Carolina, U.S., with an annual capacity of 50,000 tons. Similarly, Hunan Yuneng revealed in April 2024 its intention to establish a subsidiary in Spain, investing €129 million (RMB 982 million) to build a 50,000-ton-per-year lithium battery cathode material project.

Part 1. The rising appeal of LFP batteries

From an application standpoint, demand for LFP batteries is growing faster than the broader lithium battery industry. Industry experts highlight two key drivers:

-

Automotive Adoption: LFP batteries are gaining traction not only among Chinese automakers but also global giants like Daimler, Ford, and GM, which are increasingly integrating them into their EV lineups.

-

Energy Storage Dominance: LFP batteries’ superior safety, longevity, and cost efficiency make them the preferred choice for energy storage, where their market share is expanding rapidly.

In China, LFP batteries have already far surpassed ternary batteries in market share. Data from the China Automotive Power Battery Industry Innovation Alliance (CAPBIIA) shows that in the first three quarters of 2024, LFP batteries accounted for 68.1% (237.9 GWh) of total EV battery installations, up 43.6% year-on-year, while ternary batteries made up just 31.8% (110.9 GWh). By November 2024, LFP’s share had climbed to nearly 80%.

Overseas demand is equally robust. Chinese customs data reveals that LFP battery exports surged 26.6% year-on-year to 34.1 GWh in the first nine months of 2024, representing 36.9% of total power battery exports. In contrast, ternary battery exports fell by 6.6%.

Notably, Chinese energy storage firms secured over 80 GWh in contracts (excluding tenders) in the first half of 2024, with overseas orders exceeding 50 GWh—almost entirely for LFP batteries.

Looking ahead, global demand for LFP batteries is poised for rapid growth. Industry projections estimate Europe’s combined demand for power and energy storage batteries will reach 1,500 GWh by 2030, half of which (750 GWh) is expected to be LFP-based.

“LFP batteries offer a cost-competitive solution, enabling more affordable EVs for the middle class,” noted an executive at a major European automaker. “Their long lifespan and superior thermal stability also ensure high-quality, durable electric vehicles.”

A case in point: In July 2024, Renault placed a 39 GWh LFP battery order to power approximately 600,000 EVs. Its EV division, Ampere, is collaborating with LG Energy Solution and CATL to establish an LFP supply chain in Europe.

Part 2. Chinese manufacturers lead the charge

Industry leaders are bullish on LFP technology. Lian Yubo, Chief Scientist at BYD, asserts that “given cost and material supply constraints, LFP batteries will remain indispensable for the next 15–20 years.” Tesla CEO Elon Musk echoed this sentiment, predicting that “two-thirds of Tesla vehicles will use LFP batteries, with the remaining third relying on ternary chemistries.”

As overseas LFP capacity expands, Chinese firms are set to further dominate the global market. Analysts attribute this to their early R&D investments and first-mover advantage. With accelerated exports and overseas production, China’s LFP battery shipments are primed for explosive growth.

“For cost-effective LFP batteries, Chinese companies control over 99% of the supply chain, starting from raw materials,” an industry insider emphasized. SNE Research corroborates this, noting that “Chinese players currently dominate LFP production due to their cost edge.” As LFP-powered EVs proliferate worldwide, Chinese battery makers are rapidly solidifying their global presence.

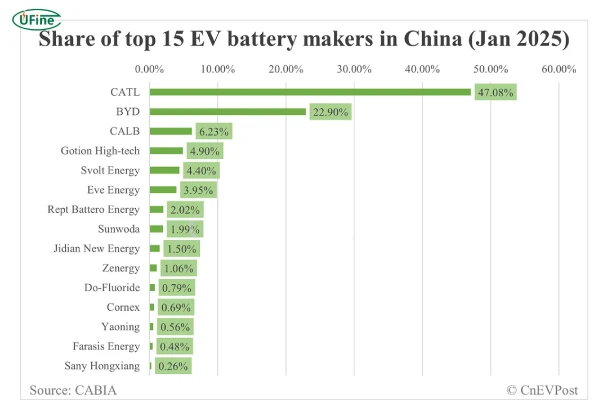

Part 3. China’s commanding share of the global LFP battery market (2024 data analysis)

China’s stranglehold on the global lithium iron phosphate (LFP) battery market has reached unprecedented levels in 2024. According to BloombergNEF’s Q4 2024 Battery Market Report, Chinese manufacturers currently control:

-

92.3% of global LFP battery production capacity

-

87.6% of worldwide LFP battery shipments (548.7 GWh out of 626.4 GWh total)

-

94% of the LFP cathode material supply chain

The China Automotive Battery Research Institute (CABRI) reveals even more granular data:

-

Capacity Distribution:

-

CATL: 185 GWh (33.7% global share)

-

BYD: 142 GWh (25.9%)

-

CALB/Gotion/EVE Energy: Combined 156 GWh (28.5%)

-

-

Export Dominance:

-

Europe received 38.2% of China’s LFP exports (13.02 GWh)

-

North America imported 28.5% (9.71 GWh)

-

Southeast Asia accounted for 21.3% (7.26 GWh)

-

Supply Chain Control Metrics (S&P Global Commodity Insights, 2024):

-

Lithium processing: 68% of global capacity

-

Iron phosphate production: 91% share

-

Cathode precursor plants: 82% located in China

Part 4. The structural advantages behind china’s LFP leadership

1. Policy-Driven Industrialization (2015-2024)

China’s strategic focus on LFP technology began with the “13th Five-Year Plan” (2016-2020), which allocated:

-

$4.2 billion in direct subsidies (Ministry of Industry and IT data)

-

Tax incentives covering 15-25% of R&D costs

-

Mandated LFP adoption in all municipal vehicle fleets by 2022

2. Vertical Integration Mastery

The complete domestic supply chain delivers 40-45% cost advantages versus foreign competitors (Benchmark Mineral Intelligence):

-

Lithium Carbonate: 53% lower production costs (<6,812/tonvs.14,560 global average)

-

Cathode Plants: 72% located within 300km of battery factories

-

Energy Efficiency: Chinese LFP plants consume 18% less power per kWh produced

3. Technology Leapfrogging

Recent breakthroughs have erased LFP’s traditional energy density disadvantages:

-

CATL’s 3rd Gen CTP Tech: 200 Wh/kg (vs. 160 Wh/kg industry average)

-

BYD’s Blade 2.0: Passes nail penetration tests at 300% higher force than NCA batteries

-

Gotion’s L600 Cell: 6,000-cycle lifespan (15% longer than 2023 models)

4. Demand-Side Economics

China’s domestic EV market creates an insurmountable scale advantage:

-

83.4% of China’s 9.7 million NEVs sold in 2024 used LFP (CAAM)

-

Battery swap stations (98% LFP-powered) grew to 3,812 locations

-

Grid-scale storage deployments reached 48.7 GWh (91% LFP share)

Projections (2030):

-

Wood Mackenzie forecasts China will maintain >85% market share

-

LFP cost advantage expected to widen to 50-55% by 2027

-

Export volumes to triple to 280 GWh annually

Part 5. Outlook

Thanks to their unbeatable cost-performance ratio and safety advantages, LFP batteries are gaining widespread acceptance overseas. With more international automakers adopting the technology, LFP is poised to secure an even more pivotal role in global markets, unlocking vast growth potential in the years ahead.

Related Tags:

More Articles

How to Choose the Best Floor Scrubber Battery for Commercial Cleaning?

Selecting the ideal floor scrubber battery ensures a long runtime, rapid charging, and minimal maintenance for efficient commercial cleaning operations.

Battery for Blower vs Battery for Leaf Vacuum: Which One Should You Choose?

Battery for blower vs leaf vacuum—learn the key differences in power, fit, and runtime to choose the right battery for your outdoor tool needs.

How to Choose the Right Battery for Blower?

Choosing the right blower battery? Consider voltage, capacity, chemistry & usage. This guide helps match the best battery for peak performance.

How to Choose the Best Insulated Battery Box for Lithium Batteries?

Choosing the Best Insulated Battery Box for Lithium Batteries? Discover key factors such as size, material, and safety for optimal protection and performance.

7 Critical Elements on a Lithium Battery Shipping Label

What must be on a lithium battery shipping label? Learn 7 key elements to ensure safety, legal compliance, and correct handling across all transport modes.

Custom Lithium-ion Battery Manufacturer